Why SPACs Are a Racket

If you like paying load fees, you’ll love special-purpose acquisition companies.

Mentioned: Digital World Acquisition Corp (DWAC), Citigroup Inc (C), Goldman Sachs Group Inc (GS), Credit Suisse Group AG (CS)

For Openers

This column is based on a paper from Michael Klausner, Michael Ohlrogge, and Emily Raun, entitled “A Sober Look at SPACs.” Their research has circulated for a while, appearing in various articles, but as the paper was updated over the holiday break, it’s worth a fresh look, particularly as the industry is once again occupying the front of the business pages, with the SPAC Digital World Acquisition Company (DWAC) preparing to merge with a firm owned by Donald Trump.

Special-purpose acquisition companies, or SPACs, are publicly traded stocks. They raise capital from seed investors, promising to invest those proceeds into a privately held company Such transactions are called “mergers.” The SPAC transfers its cash to the target in exchange for equity ownership. The private company has therefore gone public. Those who held SPAC shares through the merger now own shares in the previously private company.

Allegedly, this structure leads to a win/win/win. SPAC shareholders win by investing in the formerly privately held organizations at wholesale prices, rather than buying at an inflated value after the bigger players have flipped the merchandise. The private firms win because they acquire liquidity by going public, with underwriting costs that are claimed to be lower than with traditional IPOs. And, of course, the promoters of SPACs win, because such is Wall Street.

The promoters have indeed thrived. The companies have posted mixed results. But shareholders … sigh. Not so much.

Five Actors

Understanding the results requires appreciating each party’s role. SPACs have five performers: the sponsor, the underwriter, IPO investors, private investors, and secondary investors. The first three, broadly speaking, are the insiders who make the product. The fourth are privileged outsiders, while the fifth are nonprivileged outsiders.

- Sponsor. SPACs are typically created by Wall Streeters or by industry executives. Examples include Barry Sternlicht, who heads the $60 billion investment firm Starwood Capital, and Tilman Fertitta, CEO of the privately held hospitality firm Landry’s and owner of the NBA’s Houston Rockets.

For their efforts, sponsors receive an immense amount of free (or almost-free) SPAC shares, typically 20% of the eventual float.

- Underwriter. As with conventional IPOs, the underwriter for a SPAC is hired by the organization to distribute the initial shares. These are, in fact, the same organizations that distribute IPOs; Citigroup (C), Goldman Sachs (GS), and Credit Suisse (CS) lead the 2021 SPAC charts.

The standard underwriting fee is 5.5% of the SPAC’s initial proceeds.

- IPO Investors. This is where a SPAC differs from other stocks. Whereas traditional IPOs unofficially dole out special favors to Wall Street insiders by giving them early access to shares, SPACs make that relationship official. When SPACs issue their initial shares, they exclude the public, providing the opportunity instead to hedge funds.

Accompanying those initial shares are warrants that give the hedge funds the right to buy additional SPAC shares--usually at a large discount. In practice, the hedge funds cash out the original shares they purchase, either by reselling them to secondary investors or by redeeming them. (Before a merger closes, SPAC shareholders generally have one or two months during which they may redeem their shares at par if they wish.) Either way, the hedge funds recoup their outlays while retaining the possibility to profit through their warrants, which they have in effect been given for free, in exchange for supporting the SPAC until the time of the merger.

- Private Investors. Before a SPAC merges with a target, it usually attempts to acquire additional capital, by seeking so-called PIPE monies from private investors. (PIPE stands for "private investment in public equities.") Once again, these are institutional investors, rather than retail buyers.

Details from one PIPE to another vary considerably, but sometimes SPAC sponsors sweeten the deal, either by offering private investors discounted shares or by presenting them with warrants. (If this sounds fuzzy, so too is SPACs’ disclosure of such agreements.)

- Secondary Investors. Finally come the secondary investors. They bought their shares on the secondary market--shares originally held by the hedge funds that were the IPO investors--and have decided to retain those shares through the merger. Secondary investors consist either of retail buyers or of institutions that didn’t place higher on the SPAC ladder.

Unlike the previous parties, secondary investors do not receive special grants in the form of discounted shares, warrants, or fee payments.

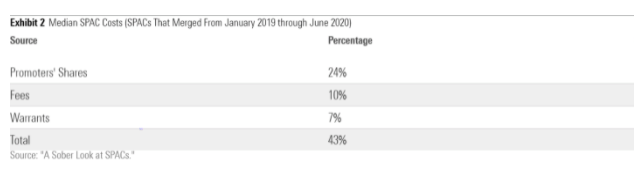

In summary:

High Costs

Secondary investors seem to have paid a very large bill. The paper's authors calculate for the 47 SPACs that were issued between January 2019 and June 2020: 1) the dilution that arises from the sponsors’ shares; 2) the various fees paid by the SPACs, underwriting and otherwise; 3) and the dilution caused by the IPO investors’ warrants. The median amounts appear below.

Talk about a load fee! For several decades, mutual fund buyers paid a maximum front-end commission of 8.5%, which the industry eventually cut to 5.5%. Even then, investors were displeased: Few fund sales today involve any front-end charge at all. Thus, while mutual fund investors balk at single-digit admission charges, secondary SPAC shareholders accept 43%.

Such is the allure of popular investments, which tempt potential buyers into overlooking the fine print. Also contributing to secondary shareholders’ willingness to foot the bill, of course, is that the charges are either implicit, or (as with the underwriting fees) paid before they purchase their shares. It doesn’t feel like a 43% hit.

Low Returns

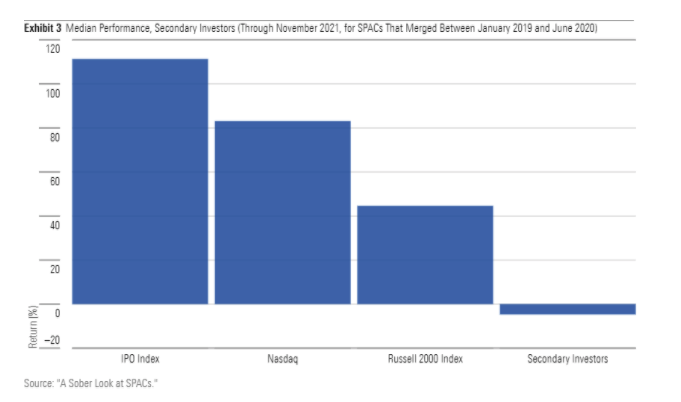

After the insiders collected their dues, secondary investors retained only $0.57 on the dollar. The good news for them was that, thanks to strong equity markets, their postmerger returns almost overcame that handicap. Through Nov. 30, 2021, the median return for the secondary SPAC investors in the authors’ database was negative 4.7%. Not an enviable result, to be sure, but impressive given how much ground that secondary shareholders initially conceded.

The bad news was the opportunity cost. While secondary SPAC investors didn’t lose much, as measured by the median result, they left a huge amount of money on the table, because other stocks were flying. Particularly successful were the stocks of companies that were most like the businesses into which the SPACs merged: small, emerging firms. The following picture may induce 1,000 tears.

The Companies’ Perspective

This all leads to the final question, of how the companies that were acquired through SPAC mergers fared. Clearly, those who promoted the SPACs profited. Sponsors received free shares; underwriters collected their fees and then departed; and IPO investors quickly recouped their outlays while retaining warrants that could pay them in the future. Equally clearly, shareholders who arrived late to the game got stuck with the bill. But what about the firms that were acquired by the SPACs? How should we consider their fates?

My initial thought was that the companies also suffered. After all, it was their stocks that lagged. But that evaluation is incomplete, because it ignores the starting point: the price at which the merger occurred. My suspicion (which the authors share) is that SPACs overpay for their acquisitions. Thus, when the postmerger stocks trail the market, that isn’t a true problem for the companies, because their initial prices were unsustainably high. The underperformance returned their stocks to their proper positions.

Unfortunately, secondary SPAC investors can take no such solace.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.